At a Glance

What is the current GST/HST rate in Canada by province?

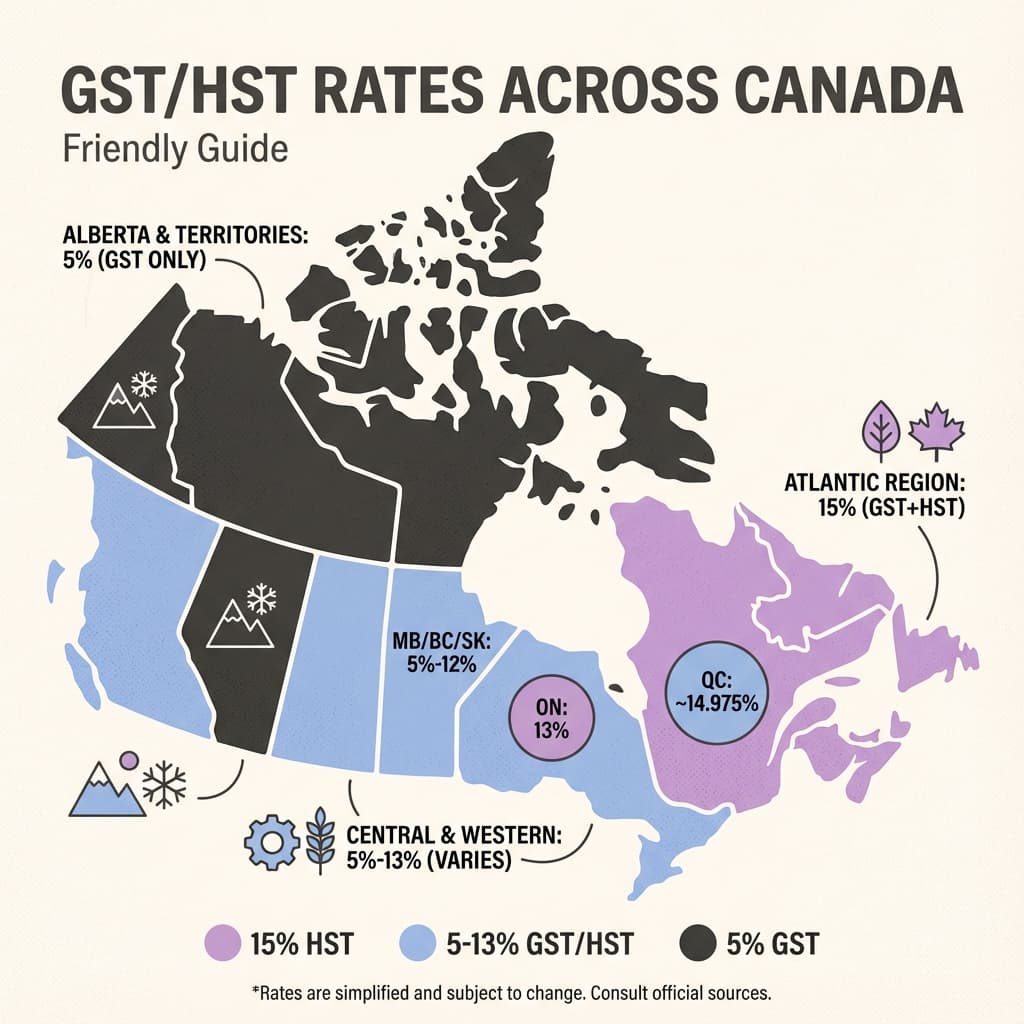

Canada's federal GST is 5% nationwide. Five provinces use a single combined HST: Ontario at 13%, Nova Scotia at 14% (reduced from 15% on April 1, 2025), and New Brunswick, Newfoundland and Labrador, and Prince Edward Island at 15%. Four provinces charge GST plus a separate provincial tax, British Columbia at 12% total (5% GST + 7% PST), Saskatchewan at 11% (5% + 6% PST), Manitoba at 12% (5% + 7% RST), and Quebec at 14.975% (5% + 9.975% QST). Alberta and the three territories (Northwest Territories, Nunavut, Yukon) charge 5% GST only. The full table by province is below.

Canada's sales tax system varies by province and territory. The federal Goods and Services Tax (GST) applies at 5% nationwide, but some provinces combine it with their provincial tax into a single Harmonized Sales Tax (HST), while others charge GST and a separate Provincial Sales Tax (PST) or Retail Sales Tax (RST).

Below is a summary of the current GST, HST, and PST rates for all 13 provinces and territories, updated for 2026, including Nova Scotia's rate reduction that took effect on April 1, 2025.

| Province / Territory | Tax Type | GST | PST / HST Provincial Portion | Total Sales Tax Rate |

|---|---|---|---|---|

| Alberta | GST only | 5% | , | 5% |

| British Columbia | GST + PST | 5% | 7% PST | 12% |

| Manitoba | GST + RST | 5% | 7% RST | 12% |

| New Brunswick | HST | , | 10% | 15% |

| Newfoundland & Labrador | HST | , | 10% | 15% |

| Nova Scotia | HST | , | 9% | 14% ⭐ |

| Northwest Territories | GST only | 5% | , | 5% |

| Nunavut | GST only | 5% | , | 5% |

| Ontario | HST | , | 8% | 13% |

| Prince Edward Island | HST | , | 10% | 15% |

| Quebec | GST + QST | 5% | 9.975% QST | 14.975% |

| Saskatchewan | GST + PST | 5% | 6% PST | 11% |

| Yukon | GST only | 5% | , | 5% |

⭐ Nova Scotia's HST rate decreased from 15% to 14% on April 1, 2025. The provincial component dropped from 10% to 9%. This was the first HST rate change in the province in 14 years.

Note: In provinces with separate GST and PST (British Columbia, Saskatchewan, Manitoba, and Quebec), the two taxes are calculated independently on the pre-tax price and appear as separate line items on receipts.

Need Help with Canadian Sales Tax?

Our CPAs handle GST/HST registration, filing, and CRA audit support for businesses across Canada.

What Is GST?

The Goods and Services Tax (GST) is a federal value-added tax applied at a rate of 5% on most goods and services sold in Canada. It is administered by the Canada Revenue Agency (CRA) and has been in effect since January 1, 1991, when it replaced the Manufacturers' Sales Tax.

The GST applies uniformly across all provinces and territories. Businesses registered for GST collect the tax from customers, then remit the net amount to the CRA after deducting any Input Tax Credits (ITCs) they are entitled to claim on their own business purchases.

Some goods and services are exempt from GST or zero-rated (taxed at 0%). Basic groceries, prescription medications, and medical devices are zero-rated, meaning businesses do not charge GST on them but can still claim ITCs on related expenses. Exempt supplies, such as residential rent, most financial services, and certain health care services, carry no GST obligation, and businesses providing only exempt supplies cannot claim ITCs.

What Is HST? Which Provinces Use It?

The Harmonized Sales Tax (HST) combines the 5% federal GST with a provincial sales tax component into a single, combined rate. Five provinces currently use the HST system:

Ontario charges HST at 13% (5% federal + 8% provincial). Nova Scotia charges HST at 14% (5% federal + 9% provincial, effective April 1, 2025). New Brunswick, Newfoundland and Labrador, and Prince Edward Island each charge HST at 15% (5% federal + 10% provincial). The CRA publishes the official current GST/HST rate tables and updates them when provinces make changes.

The advantage of HST for businesses is simplicity: you collect and remit one tax instead of two. Businesses registered for HST can claim ITCs on the full HST paid on eligible business expenses, which is not always the case with separate provincial taxes.

For consumers, the HST applies to the same base of goods and services as the GST. The provincial component of HST generally follows the same exemptions and zero-rating rules as the federal portion, though some provinces offer additional point-of-sale rebates on specific items such as children's clothing and books.

PST, RST, and QST: Provinces with Separate Provincial Tax

Four provinces maintain their own provincial sales tax systems separate from the federal GST. These taxes are administered by the provinces themselves (or, in Quebec's case, by Revenu Québec), not by the CRA.

British Columbia charges a 7% Provincial Sales Tax (PST) on top of the 5% GST. BC's PST applies to most goods and some services but is not a value-added tax, businesses generally cannot claim credits for PST paid on their own purchases. Notable BC PST exemptions include basic groceries, prescription medications, children's clothing, and books.

Saskatchewan levies a 6% PST alongside the 5% GST. Saskatchewan's PST applies broadly to goods and certain services, including digital products.

Manitoba applies a 7% Retail Sales Tax (RST) on top of the 5% GST. As of January 1, 2026, Manitoba's RST expanded to cover cloud computing services, software subscriptions, data storage, and remote computer processing, aligning the province with BC and Ontario in how it taxes digital services.

Quebec charges a 9.975% Quebec Sales Tax (QST) alongside the 5% GST. Quebec's tax system is unique in that Revenu Québec administers both the federal GST and the provincial QST for most Quebec-based businesses, meaning businesses deal with one agency for both taxes. QST functions as a value-added tax similar to GST, so registered businesses can claim input tax refunds on QST paid on business purchases.

For a deeper look at how sales tax interacts with e-commerce operations in Canada, including place-of-supply rules and multi-province selling, see our e-commerce GST/HST guide.

How to Calculate GST/HST on a Purchase

Calculating sales tax depends on whether you are in an HST province or a province with separate GST and PST.

In an HST Province (Single Tax)

Multiply the pre-tax price by the HST rate.

Example, Ontario (13% HST): A consulting invoice for $5,000 before tax:

$5,000 × 0.13 = $650 HST

Total: $5,650

Example, Nova Scotia (14% HST): A $200 appliance purchase:

$200 × 0.14 = $28 HST

Total: $228

In a Province with Separate GST + PST (Two Taxes)

Calculate each tax separately on the pre-tax price, then add both to the total.

Example, British Columbia (5% GST + 7% PST): A $1,000 piece of office furniture:

GST: $1,000 × 0.05 = $50

PST: $1,000 × 0.07 = $70

Total: $1,120

Example, Quebec (5% GST + 9.975% QST): A $500 software subscription:

GST: $500 × 0.05 = $25

QST: $500 × 0.09975 = $49.88

Total: $574.88

Note that in Quebec, QST is calculated on the pre-tax price (not on the price plus GST). This changed in 2013 when Quebec aligned its QST calculation base with the GST.

If your business needs help setting up automated tax calculations, Xero handles multi-province GST/HST rates automatically and maps them to the correct accounts in your chart of accounts. New Canadian businesses can get our Xero offer to automate this from day one. See our accounting software comparison for other options.

Recent Changes: Nova Scotia HST Reduction in 2025

On April 1, 2025, Nova Scotia became the first HST province to change its rate in 14 years, reducing the HST from 15% to 14%. The provincial component decreased from 10% to 9%, while the federal 5% GST portion remained unchanged.

This change was announced by Premier Tim Houston on October 23, 2024, as part of a broader effort to address cost of living concerns in the province. The reduction is projected to decrease provincial revenues by approximately $261 million in the 2025-26 fiscal year.

What businesses need to know: The CRA published transitional rules (GST/HST Notice 342) covering how the rate change applies to transactions that straddle the April 1, 2025 effective date. The general rule is that the applicable rate depends on when the consideration for a supply becomes payable, not when the goods or services are delivered. Consideration that became due or was paid before April 1, 2025 is subject to the old 15% rate. Consideration that becomes due on or after April 1, 2025, without having been paid before that date, is subject to the new 14% rate.

Businesses operating in Nova Scotia should have already updated their point-of-sale systems and accounting software. If you are still using the old 15% rate, this needs to be corrected immediately. Our tax compliance team can review your configuration to ensure accuracy.

GST/HST Registration: When Do You Need to Charge Tax?

Businesses must register for a GST/HST account if their total taxable supplies exceed $30,000 over four consecutive calendar quarters or in a single calendar quarter. Once you exceed this threshold, you have 29 days to register with the CRA.

Below the $30,000 threshold, your business is considered a "small supplier" and is not required to collect GST/HST. However, voluntary registration is permitted and can be beneficial, particularly for businesses with significant startup costs, as registration allows you to claim ITCs on GST/HST paid on business purchases.

Key registration facts: One GST/HST registration covers you across all of Canada. You do not need separate registrations for each province. However, if you sell in provinces with separate PST systems (BC, Saskatchewan, Manitoba), you may need additional provincial registrations. Quebec requires a separate QST registration through Revenu Québec.

The CRA's Business Registration Online (BRO) portal is the primary method for new GST/HST registrations.

For a complete walkthrough of the registration process, see our guide on when and how to register for GST/HST.

GST/HST Filing and Remittance Deadlines

Your filing frequency depends on your annual taxable supplies. The CRA assigns your reporting period based on your revenue at registration, and it adjusts automatically as your revenue changes.

Annual taxable supplies under $1.5 million: File annually. Your return and any balance owing are due three months after the end of your fiscal year.

Annual taxable supplies from $1.5 million to $6 million: File quarterly. Your return and payment are due one month after the end of each fiscal quarter.

Annual taxable supplies over $6 million: File monthly. Your return and payment are due one month after the end of each reporting period.

Regardless of filing frequency, you can choose to make instalment payments to spread the burden across the year rather than paying a lump sum at year-end.

For a detailed walkthrough of the filing process, including how to use the CRA's NETFILE system, see our step-by-step GST/HST filing guide.

Zero-Rated vs. Exempt Supplies

Not all goods and services are taxed at the standard GST/HST rate. Understanding the distinction between zero-rated and exempt supplies is important for both businesses and consumers.

Zero-rated supplies are technically taxable, but at a rate of 0%. This means no GST/HST is charged to the customer, but the business can still claim ITCs on expenses related to producing or supplying these goods. Key zero-rated items include basic groceries (fresh fruits, vegetables, meat, dairy, bread, and similar unprocessed foods), prescription medications, medical devices prescribed by a practitioner, and exports of goods and services.

Exempt supplies are not subject to GST/HST at all. However, businesses providing only exempt supplies cannot claim ITCs on related expenses. Common exempt supplies include most health and dental services provided by licensed practitioners, residential rent (for periods of one month or more), most financial services (including interest, insurance premiums, and investment management fees), childcare for children under 14, and most educational services provided by recognized institutions.

The distinction matters for business owners: if you sell zero-rated supplies, you can recover your input taxes. If you sell exempt supplies, you cannot. This can significantly affect your cost structure and pricing. For a comprehensive list of HST exemptions in Ontario specifically, see our Ontario HST Exemptions guide.

Input Tax Credits: How Businesses Recover GST/HST

Registered businesses can recover the GST/HST they pay on eligible business purchases through Input Tax Credits (ITCs). This is a core advantage of the value-added tax system, the tax is ultimately borne by the final consumer, not by businesses in the supply chain.

To claim ITCs, you must be a GST/HST registrant, have paid or owed GST/HST on a purchase used in your commercial activities, and have adequate documentation (typically an invoice showing the supplier's GST/HST number, the amount of tax paid, and the date). Receipt management tools like Dext can automatically extract GST/HST amounts from invoices and receipts, ensuring you capture every eligible ITC.

Some expenses have restricted ITC eligibility. Meals and entertainment expenses, for example, are limited to a 50% ITC claim. Personal-use portions of mixed-use assets (such as a vehicle used for both business and personal travel) must be prorated.

The GST/HST Quick Method offers an alternative for small businesses with taxable supplies of $400,000 or less. Instead of tracking every ITC, you remit a set percentage of revenue, which can simplify your bookkeeping considerably and sometimes results in tax savings.

GST/HST for Digital and Remote Services

Since July 1, 2021, non-resident businesses selling digital services to Canadian consumers must register for GST/HST if their Canadian revenues exceed $30,000 annually. This applies to streaming services, software subscriptions, online courses, e-books, and other digital products.

For Canadian businesses providing remote services to clients in other provinces, the place-of-supply rules determine which rate applies. Generally, the rate is based on the province where the customer is located, not where the service provider operates.

This is particularly relevant for businesses operating across multiple provinces. A consulting firm based in Alberta (5% GST) serving clients in Ontario must charge 13% HST on services delivered to Ontario-based clients. Getting this wrong can lead to reassessments from the CRA.

For more on how GST/HST applies to digital businesses and cross-border scenarios, see our guide on GST/HST on remote services.

Frequently Asked Questions

What is the current GST/HST rate in Canada in 2026?

The federal GST is 5% nationwide in 2026, unchanged since 2008. In the five HST provinces, the combined rate ranges from 13% (Ontario) to 15% (New Brunswick, Newfoundland and Labrador, Prince Edward Island), with Nova Scotia now at 14% after the April 1, 2025 rate cut.

Did the Nova Scotia HST rate change in 2025?

Yes. Nova Scotia's HST rate decreased from 15% to 14% on April 1, 2025, the first HST rate change in the province in 14 years. The provincial component dropped from 10% to 9%, while the 5% federal GST portion stayed the same. The CRA published transitional rules (GST/HST Notice 342) for transactions that straddle the effective date.

Which provinces use HST and which use GST plus PST?

Five provinces use HST (Ontario, Nova Scotia, New Brunswick, Newfoundland and Labrador, Prince Edward Island), four charge GST plus a separate provincial tax (British Columbia, Saskatchewan, Manitoba, Quebec), and the remaining four jurisdictions charge GST only (Alberta, Northwest Territories, Nunavut, Yukon).

Which Canadian province has the lowest sales tax?

Alberta and the three territories (Northwest Territories, Nunavut, Yukon) have the lowest sales tax in Canada at 5% (federal GST only, no provincial sales tax). Among provinces with a provincial component, Saskatchewan is lowest at 11% combined (5% GST + 6% PST).

Which Canadian province has the highest sales tax?

The three Atlantic HST provinces, New Brunswick, Newfoundland and Labrador, and Prince Edward Island, share the highest combined sales tax at 15% (5% GST + 10% provincial component). Quebec is close behind at 14.975% (5% GST + 9.975% QST).

What is the difference between GST and HST?

GST is the 5% federal tax that applies across all of Canada. HST combines the federal GST with a provincial sales tax into a single rate, used in five provinces: Ontario (13%), Nova Scotia (14%), New Brunswick (15%), Newfoundland and Labrador (15%), and Prince Edward Island (15%). In HST provinces, businesses collect one combined tax rather than two separate taxes.

What is the HST rate in Ontario?

Ontario's HST rate is 13%, consisting of the 5% federal GST and an 8% provincial component. This rate has been in effect since Ontario adopted HST on July 1, 2010.

What is the sales tax rate in British Columbia?

British Columbia charges 12% in combined sales tax, made up of 5% federal GST and 7% provincial PST. The two taxes are calculated separately on the pre-tax price and appear as separate line items on receipts. BC's PST is not a value-added tax, so businesses generally cannot claim credits for PST paid on their own purchases.

What is the sales tax rate in Manitoba?

Manitoba charges a combined 12% sales tax, made up of 5% federal GST and 7% provincial Retail Sales Tax (RST). These are charged as two separate taxes. As of January 1, 2026, Manitoba's RST also applies to cloud computing services, software subscriptions, and data storage.

How do you calculate HST on a purchase?

Multiply the pre-tax price by the HST rate. For example, a $100 purchase in Ontario (13% HST): $100 × 0.13 = $13 HST, for a total of $113. In provinces with separate GST and PST, calculate each tax separately on the pre-tax price.

Do I need to register for GST/HST?

You must register if your business earns more than $30,000 in taxable supplies over four consecutive calendar quarters or in a single calendar quarter. Businesses below this threshold are considered small suppliers. Voluntary registration is permitted and can be beneficial for claiming ITCs. See our full GST/HST registration guide for details.

What items are GST/HST exempt in Canada?

Key exempt items include basic groceries, prescription medications, most medical devices, most health and dental services, childcare services, residential rent, and most financial services. For a detailed list of Ontario-specific exemptions, see our Ontario HST Exemptions List.

This article is current as of February 2026. Tax rates and thresholds can change, always verify with the CRA or a Chartered Professional Accountant before making business decisions. This content does not constitute professional tax advice. If you need help managing GST/HST compliance for your business, our bookkeeping team can handle your filings and ITC claims.

Seb ProstCPA, Ex-CRA

Licensed CPA with 10+ years of experience, including work with the Canada Revenue Agency. Founder of LedgerLogic, a cloud accounting firm serving Canadian SMEs. Xero Certified Advisor.